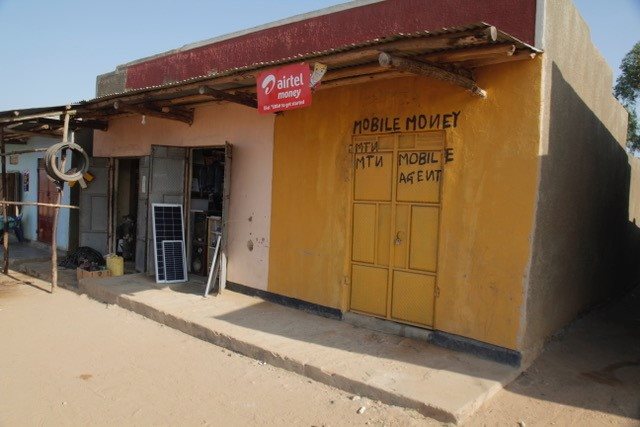

Uganda is one of the East Africa leaders in mobile money since the introduction of the first digital wallets in 2009. The offering of digital financial services is evolving from basic airtime top-ups and money transfers to more advanced products such as bulk payments, merchant payments, as well as savings and credit products.

However, the market is still grappling with how to meaningfully serve rural areas beyond basic payments. MM4P started its work in 2015 launching a public-private Digital Finance Working Group that improved the communication among providers and between them and the regulator. The long-awaited amendment to the Financial Institutions Act was passed by the Parliament in January 2016 and gazetted in 2017, enabling banks to provide agent banking services.

Since 2015, MM4P has helped banks prepare for agency banking and is now supporting five to enter the market. MM4P assisted in the pilot and launch of MoKash, the first digital credit service, which registered several million active clients since its launch in 2016. MM4P has heavily focused on going rural, working in value chains to digitize payments from off-takers to farmers, which included supporting the recruitment, set-up and management of rural agents. In doing so, MM4P has partnered with fintech companies to aggregate payments, manage agents and provide additional services connected to digital payments, including solar kits and door-to-door health and medical products. Uganda has also played host to MM4P two large partner events, #DFSgoRural and #DFS4Women, bringing in over a hundred partners from around the globe.

MM4P is generously supported by the Bill & Melinda Gates Foundation and the Government of Belgium for its work in Uganda.